Anyone Can Be An Activist Investor

And Everyone Must!

In our earlier series on using financial leverage in the fight for a livable planet, I present the case for using financial investment in fossil fuel companies to exert pressure from the inside and force movement to a decarbonized feature. There is growing awareness of the need for this strategy.

A recent academic paper out of The National Bureau of Economic Research titled “Counterproductive Sustainable Investing” says:

“…sustainable investing that directs capital away from brown firms and

toward green firms may be counterproductive, in that it makes brown firms more brown without making green firms more green.”

Activists are starting to use their shareholder position to force conversations with corporate management and in the courts.

This series epilogue provides a straightforward road map so every climate stakeholder, of any means, can be involved in this crucial movement.

What’s driving this push is simple: People are dying because of global heating. Fossil fuel emissions continue to increase. Ecosystem destruction bulldozes peoples’ lives. For thirty years, climate activists have been trying to stop the devastation. It’s not working.

Roughly $100 billion dollars has been poured into “climate philanthropy” over the last 30 years [note 1] and we’re not getting our money’s worth. The reason is simple: money, the most powerful energy source on the planet, has not been used to take control of how energy companies are run.

By taking more ownership and control of the fossil fuel industry we will structurally address how Big Oil does business. We need to charge straight into the heart of battle and buy shares of oil company stock, putting financial resources into direct laser-focused engagement with climate-destroying companies.

This idea is shocking to a generation of activists who grew up with calls to divest from fossil fuel and think that buying oil companies’ stock supports or enables them [note 2.] But influence over corporate behavior is achieved using financial muscle and divestment alone isn’t getting the job done.

If we had bought $100 billion dollars’ worth of shares in fossil fuels companies to acquire 5% ownership stakes, we would wield massive influence over $2 trillion worth of all oil and gas companies, controlling roughly 30% of annual emissions. We’d be within shouting distance of the Paris Agreement goals: “Emissions need to be reduced by 45% by 2030.”

Consider:

Five percent ownership in a company influences corporate board elections, mobilizes other shareholders, and creates an enormous amount of awareness.

Five percent ownership by pro-climate activist investors is five percent not controlled by regressive, uncaring, or ignorant investors.

Five percent ownership in a company means the CEO answers the phone personally when investors call.

This is the power of shareholder activism.

The potential to exert this much influence can’t be ignored. Anyone can, and everyone must become an activist investor and add a crucial tool to their climate action toolbox.

Here are some paths to investor action, for anyone, at any level of commitment and capability.

Spread the Word, Become Informed

As You Sow is arguably the most prominent and powerful organization advocating for pro-social change through shareholder engagement and has a long list of needle-moving successes to show for it.

Their page on shareholder advocacy talks about why it is so effective compared to other types of action. Armed with this information, you’re better able to talk about this approach with others, especially people who are skeptical and are only used to hearing about divesting.

Hands-Off, Simplest Action: Buy a Single Share through Follow This

For about $11 (10 euros) you can cast a vote at Shell’s shareholder meetings.

Follow This lets you buy a share in Shell, British Petroleum, Total Energies, Exxon, or Chevron. With the shares you and others have purchased, they vote on or submit shareholder proposals, influencing companies to decarbonize and mitigate climate damage.

Follow This’ Buy-A-Share page has a description of how the shareholder voting process works and links to buy your share. Get 10 friends to follow your lead and you have made a significant step in building a mass movement.

Nothing else is required on your part if you choose this path.

New to Investing? Open a Basic Investment Account

To directly vote in corporate elections you must own stock. Thanks to mobile stock trading platforms, social media investment groups, and programs connecting shareholders to corporate voting ballots, this is easier than ever.

Robinhood may be the most well-known, and easiest, reputable stock investment platform for the starting investor. There are others if you want to research various features, as you would when picking any financial services provider such as your bank.

An account can be opened with any amount of money, and the sign-up process takes perhaps half an hour. It takes a couple of days after that to confirm a connection to a bank account.

Then you’re ready to be an activist investor.

Vote the Shares You Own

As an activist investor, choose which companies require your attention. Weigh how much money you want to dedicate and how much shares cost, then buy your shares. With shares in your account, it’s time to engage.

Put corporate voting on autopilot with As You Sow’s Vote Your Values. That page directs you to the Iconikplatform where you create a login to get started.

Once you are connected to Iconik, their system will automatically vote your shares at your companies’ annual meetings in accordance with the pro-social and decarbonization-focused As You Sow ESG-aligned proxy voting guidelines.

The voting profile defines two principles, which guide how your vote is cast:

- Shareholders should have a say on climate change issues

- Companies should make all possible efforts to limit their negative impacts on climate change

Profits made from your investments can be used to increase your ownership stake and voting power or can be donated to an organization like As You Sow. Use any profits a company generates to fund efforts to mitigate the damage they do.

You can also sign up to Troop and join other activists in voting campaigns.

If You Own ETF’s and Mutual Funds

As You Sow and other groups are fighting complex and expensive battles for your rights to exercise control over the companies in your ETF and mutual funds’ holdings. Because this type of shareholder “pass-through” voting threatens the status quo, it is being resisted.

Investors should contact their ETF and mutual fund management and insist they pay attention to how you want them to vote. Blackrock and Vanguard are both experimenting with how to operationalize some pass-through voting so fund holders can exert their influence. Stay informed. This will happen but outreach is critical.

Another alternative is to move your fund positions to Engine No. 1, which runs two ETF’s that directly engage with corporate management, pushing them to change from within.

Resist the temptation to ignore your funds or just select funds that call themselves “sustainable” or “ESG-focused.” This is giving up voting power where it’s needed the most, and leaves incumbents in place to continue climate destruction.

Activist Investing with Your Retirement Plan

Retirement plans hold trillions of dollars of individuals’ investments, and therefore potentially wield a tremendous amount of economic power. Urge your workplace plan to support shareholder voting - become an activist by engaging your employer and making administrators aware of your position on sustainability and shareholder democracy.

As You Sow’s “Invest Your Values” page lets you research funds that may already be in your employer’s plan. From there, the “Get Started” button takes you to a page with five concise action items to start influencing your company’s plan options.

Your company’s plan defaults may already be scored for how they align with pro-social and low-carbon goals. For example, Whole Foods, Inc. default “Target Date” retirement fund scores only “fair” or “poor” across all categories of As You Sow’s profile. Until the large funds like Blackrock and Vanguard connect fund owners to votes, the focus remains on selecting funds that avoid polluting companies.

Tell administrators where they can directly learn more and take action, and claim the right to vote your ownership stakes.

Working with an Investment Advisor

If you work with an investment advisor, make them aware of your preferences to become actively involved with voting your shares and direct them to As You Sow’s “Institutional Investor” page.

Also tell your manager about Iconik, which provides a service to connect the manager’s clients (you) to the Iconik voting technology.

As a fund manager’s client, you are in control. If your fund manager is not responsive to your preference to vote your shares in alignment with your values, find another advisor who is.

Conclusions

The “climate movement” has invested $100 billion plus on stopping climate destruction and it hasn’t worked – most industry response to political and social pressure has been window-dressing to create an impression of climate action, while emissions and damage continue to grow.

But:

Every share of oil company stock is a vote on how it is run, who runs it, and how its mission will benefit its shareholders. Stock ownership doesn’t enable or enrich a company – it entitles the stockholder to have a voice. We need to be that voice.

Every share of oil company stock that’s divested, or passively ignored while people are busy elsewhere, is a vote for status-quo climate destruction.

Every climate advocate can help control the behavior of the companies that are destroying our planet by stepping up and stepping in, showing up in the boardroom with dollars and votes.

There is an action roadmap for anyone, at any level of involvement, to follow. All you need to do now is choose your path and take that first step to exercise your power.

Strength is in numbers. As with any mobilization, the network effect is needed to scale up activist investing and every conversation is an opportunity to create awareness of the potential of investment power. Climate Action Now will soon be hosting actions that will allow everyone to send a message to employers, fund managers, and company management: “as financial stakeholders in these companies we insist on a voice and demand action.” Stay tuned!

Footnotes:

Note 1: According to Inside Philanthropy, “climate change giving [in 2021 reached] between $7.5 billion to $12.5 billion” not counting contributions from millions of individuals. My estimate is based on these numbers, estimating 2022 at $10B and 2021 at $7.5B, and assuming the overall philanthropic giving growth rate of 8% annually back to 1990.

Note 2: A company sells (“issues”) stock shares and gets paid for them only once. After that, stock price changes affect the investors who own the shares - not the company directly. Companies are indirectly affected because executive compensation is tied to stock prices. But this is very uncertain and inefficient – firing executives for stock underperformance rarely happens. The real control over company behavior is held by the Board of Directors, and investors directly vote the Board members in or out. That’s where power must be focused.

What is the Most Valuable Thing in the Entire World? The Cap and Trade Shell Game: Unproven System Bets The Atmosphere

What is the Most Valuable Thing in the Entire World?

The Cap and Trade Shell Game: Unproven System Bets The Atmosphere

“What is the most valuable thing in the entire world?”

“The head of a dead cat.”

“Why?”

“Because nobody can put a price on it.”

- Zen Parable from Zen Buddhism Stories, Trout Lake Media

For over a decade, academics have been touting “Cap and Trade” (C/T) and a carbon credits trading market as the best way to achieve GHG emissions reductions without the extremes of full government regulation and complete inaction.

Although emissions trading has been claimed to be successful in the case of mitigating acid rain and leaded gasoline pollution, C/T:

- Has not been shown to be effective in reducing GHG emissions.

- Has been engineered by academics indoctrinated into the beliefs of a market system that makes so-far-unproven claims of optimality.

- Can only ever be as effective as the assumptions underlying it are accurate and complete.

Put another way, C/T is a complex system of financial engineering with the stated goal of managing emissions levels by establishing the right market conditions, while in fact it’s also designed not to make anyone angry, especially the global petroleum industry and moneyed free marketeers.

A brief overview of Cap and Trade

In a cap-and-trade system, the government sets a limit (“cap”) on permissible emission levels and allocates pollution allowances among the industry participants which allow them to emit their pollutants up to the capped level.

Some allowances are freely allocated while others are sold at Government auctions. They can also be bought and sold in the secondary carbon trading market. In theory this system provides incentives for finding low-cost methods to reduce emissions to meet the cap. If unable to meet the cap the polluters must purchase allowances.

In theory this will result in overall pollution reduction. The rationale is based on many assumptions, including:

- If a company produces a higher level of emissions than their allocated or purchased permits allow, they are taxed and can be penalized for the violation. On the flipside, a company that reduces their emissions can sell their allowances to other companies that pollute more. Or “bank” the credits for future use.

- Each year, the Government lowers the number of permits that are issued and therefore lowers the total emissions cap. As a result, permits get more expensive. Over time, companies have an incentive to reduce their emissions more efficiently and the logic is that they would benefit from investing in clean technology as it becomes cheaper than buying permits.

A toy illustration of Cap and Trade:

Stripped to its bare bones, C/T looks something like this:

Say Alice has a widget factory that emits 200 units of CO2. She has a cap of 150 units but also wants to lower her fuel bill and do a good thing for the atmosphere by installing a solar array for $1000 that cuts her emissions in half, to 100 units. She’s now under her cap and has 50 units she can trade as credits to someone else, to help pay for the solar installation.

Bob has a power plant that emits 1000 units of CO2, but his cap is 950 units. The fuel he uses is so polluting it will cost $5000 to mitigate the excess 50 units. Bob goes to the open market and sees Alice’s 50 units for sale. The magic, invisible hand of the market will establish the right price for those fifty units so that Alice gets a reduction in her capital outlay for the solar panels, and Bob …. Gets to keep emitting.

So Bob will continue to pollute, and nullify any environmental benefit from Alice’s renewable energy investment, until the Government manipulates the prices of emissions units to make it more expensive to purchase the credits than to install mitigations. This shell game where mitigations in one place are just transferred to unmitigated emissions elsewhere is quaintly termed “the waterbed effect” by economists.

What could possibly go wrong?

From this toy model, start plugging in other parameters: Government-defined fines for excess emissions. Government-defined incentives for clean energy innovators to produce lower cost solutions. Government-defined price floors so credits don’t become so cheap they aren’t of any value to emissions reducers. Government-defined price ceilings so the credits don’t become so expensive the polluters get angry.

How do you balance fines and the price ceiling? How do you keep the market “fair” and mitigate asymmetries between the participants? How do you police collusion? Where does the Government set floor and ceiling prices? And Government intervention? Industry hates that, and if there’s to be Government intervention, why not cut to the chase and mandate GHG reduction via a carbon tax? Because industry hates that too.

Then there’s what this looks like to implement. The current regulation document is 450 pages long, and contains poetic passages like:

“§ 95853. Calculation of Covered Entity’s Full Compliance Period Compliance

Obligation.

(a) A covered entity that exceeds the threshold in section 95812 in any of the four data years preceding the start of a compliance period is a covered entity for the entire compliance period. The covered entity’s full compliance period compliance obligation in this situation is calculated as the total of the emissions with a compliance obligation that received a positive or qualified positive emissions data verification statement or were assigned emissions pursuant to section 95131 of MRR from all data years of the compliance period.

(b) A covered entity that initially exceeds the threshold in section 95812 in the first year of a compliance period is a covered entity for the entire compliance period. The covered entity’s full compliance period compliance obligation in this situation is calculated as the total of the emissions that received a positive or qualified positive emissions data verification statement or were assigned emissions pursuant to section 95131 of MRR from all data years of the compliance period.

(c) A covered entity that initially exceeds the threshold in section 95812 in the second year of a compliance period is a covered entity for the second and any remaining years of this compliance period. The covered entity’s full compliance period compliance obligation in this situation is calculated as the total of the emissions that received a positive or qualified positive emissions data verification statement or were assigned emissions pursuant to section 95131 of MRR for the second and any remaining data years of the compliance period.

(d) A covered entity that initially exceeds the threshold in section 95812 in the final year of a later compliance period has a compliance obligation for its emissions that received a positive or qualified positive emissions data verification statement or were assigned emissions pursuant to section 95131 of MRR for that year, but the entity’s full compliance period compliance obligation for the current compliance period is not due the following year. Instead, the entity’s reported and verified or assigned emissions for this year will be added to the entity’s full compliance period obligation for the subsequent compliance period”

Not that our technocracy can’t handle complex systems. The Internet. The moon landing, James Webb telescope, & Large Hadron Collider. The multi-trillion-dollar global financial system. “Can we build it? Yes, we can! Most of the time….” – but there are important differences between building those technologies and tackling existential threats to survival.

Humans are likely to survive a meltdown of the Internet or the global financial system. The outcome of failing to mitigate climate is much more uncertain and the tail risk (even if very low probability) is extinction (infinite harm) or de-civilization (almost infinite.) So, is this Cap-and-Trade contraption the best way to reduce GHG emissions to maintain a habitable climate and global ecosystem within the limited time we have?

The bugs in the system are in fact features, machinations designed to satisfy the needs of the owners of the modern western industrialized consumer economy, who are only willing to mitigate environmental destruction if it satisfies shareholders.

This is discussed at length in a recent paper, “California’s ambitious greenhouse gas policies: Are they ambitious enough?” The paper is a deep dive into the myriad details of what can go wrong, or is already wrong, with C/T, deconstructing the perverse logic that gives us “the waterbed effect” and other counterproductive results.

It urges policy makers to devise a statewide plan that directly supports decarbonization across the entire economy, rather than the myopic (failed) market-price-based carbon mitigation approach more palatable to corporations.

A statewide decarbonization project on the scale and scope required for climate stabilization may be too big a job for CARB or the California government to take on.... Regulatory policy should accommodate, facilitate, and help coordinate complementary and independent climate actions in support of the state’s climate goals; it should not undermine and discourage such actions by nullifying their environmental benefits. A core objective of state policy should be to empower individuals, businesses, communities, and municipalities to influence the scale and pace of decarbonization through their collective actions and investment choices, and to reap the economic dividends accruing from their choices.

The Head of a Dead Cat

What does all this have to do with the Zen parable?

Not only does C/T as designed impede or deadlock decarbonization, but the most critical input to its economic model is also missing. Nowhere in the design of C/T economics is any value given to breathable air, manageable climate and weather, or any other natural resource. You can’t design a truly meaningful system to trade on the right to degrade the conditions under which all creatures have lived for the last tens of thousands to millions of years.

The best our industrialized academics have devised to price the habitable world is a thing called “The Social Cost of Carbon” (SCC.) An Internet search on this phrase will return pages and pages of studies – created by more of the same academics, economists, and industrialists who gave us C/T – in which they attempt to come up with a metric that someday can be plugged into equations of climate-survivability-as-long-as-it-doesn’t-cost-money.

But California’s C/T system design, just like the California electrical net-metering NEM3 design, doesn’t even attempt to include this. There is no SCC analysis in California’s C/T regulations.

The consulting firm E3 plays a conspicuous role in the climate-vs-economics modeling behind not only NEM3 and C/T for California but much of the country, yet the industrial-political-economic complex cannot put a price on the head of a dead cat, the air we breathe, the water we drink, or a survivable temperature range. The financial design philosophy behind C/T ignores the most valuable things in the world.

Call to Action

Public comment is closed, and the legislation is finished, so the work ahead is to exert influence on legislatures and CARB to evolve their vision of how decarbonization is best achieved, over the longer term.

Climate Reality members can be part of this effort by

- Subscribing to the C/T program email updates here.

- Reaching out to CARB members listed here and reporting on what they have to say about missteps and omissions mentioned here.

- Reaching out to E3’s Tory Clark or email E3 at [email protected] and see if there are answers to some of the hard questions.

- Reaching out to CARB’s Market Advisory Committee to vigorously lobby for changes due to the biases and omissions in the current plans.

- Reaching out to your legislators – though they have less influence over C/T and have delegated their responsibility to CARB.

And as always, post your leadership actions on the Hub!

Afterword

For more on whether California’s C/T plans include SCC criteria, Microsoft’s AI-powered search returned this result:

“According to the web results, California’s cap and trade regulation does not explicitly include “social cost of carbon” analysis. The social cost of carbon (SCC) is an estimate of the cost of the damages created by one extra ton of carbon dioxide emissions1. It is used to evaluate the benefits and costs of policies that affect greenhouse gas emissions2. California’s cap and trade program is designed to achieve the maximum feasible and cost-effective reductions in California greenhouse gas emissions3, but it does not use the SCC as a direct input. Instead, it sets a limit on emissions and allows regulated entities to trade allowances and offsets within that limit4.

Learn more

1. en.wikipedia.org 2. news.stanford.edu 3. arb.ca.gov 4. arb.ca.gov 5. edf.org 6. arb.ca.gov 7. carboncredits.com

Protest, Punish, or Participate?

Big Oil can be bought.

This is the third and last in our series of posts about the role of financial strategies in shaping climate policy and the energy industry. The first article was a quick overview of how divestment and investment mechanics operate in influencing corporate behavior. The second was a critical look at how divestment strategy has played out. Now, in this article I make the case that the best way to accomplish our climate goals is with active, vigorously engaged investment rather than by protest, reliance on ESG promises, or divestment.

News happens fast. Just since starting to write this piece there have been major events that affect and shape the climate destruction discussion. In Davos, Al Gore exhorted the panel that the world isn’t doing enough and we’re moving too slowly. The points I made in the previous article about protest and divestment provide some clues as to why this might be the case.

But before Davos, a surprising example of how an aggressive use of money can change the shape of an entire industry unfolded: Elon Musk’s takeover of Twitter. Ignoring the accompanying theater and ruckus, when all was said and done a major social media enterprise was restructured, refocused, and reinvented according to the desires of a small group of stakeholders. The transformation began the moment ink was dry and major disruption followed.

As a thought experiment, then, consider: Occidental Petroleum has a total market value of about $55 billion. According to Wikipedia, “Occidental had 2.911 billion barrels of oil equivalent (1.781×1010 GJ) of oil equivalent net proved reserves, of which 51% was petroleum, 19% was natural gas liquids, and 30% was natural gas. In 2020, the company had production of 1,350 thousand barrels of oil equivalent (8,300,000 GJ) per day.[3]”

What would happen if a consortium of “climate preservation” interests raised sufficient capital to take Occidental private, and reinvent the petroleum company? It’s only 10% of the size of Exxon-Mobil but a takeover of Occidental would be a seismic event that would change the petrochemical industry forever, with implications far larger than just a change in the management structure of a middling fossil fuel company. That’s real leverage.

Continuing the thought experiment, if Occidental’s fossil fuels were left in the ground, the cost of sequestering the associated greenhouse gasses would be about $44/ton assuming the company were just liquidated. According to the International Energy Agency, carbon capture can cost anywhere from the neighborhood of $15/ton for some pure CO2 streams, to more than $100/ton. The Center for Climate and energy Solutions estimates forest sequestration costs to be in the range of $30 to $90 per ton. In other words, the radical notion of buying oil companies for the purpose of not pumping the oil is competitive with the costs to continue using the atmosphere as a sewer while trying to clean up after the mess.

Far-fetched? Sure. Gargantuan forces would need to be marshalled to accomplish such a task. Also, we can’t wait for a hypothetical Elon Musk to show up and start to reconfigure the fossil fuels industry (although, when you consider the trillions of dollars in climate damage occurring – direct costs and investment in mitigation – $55B is a drop in the barrel and might seem cheap to some visionary.)

This thought experiment is fanciful, but the truth is that the globe operates on a version of “The Market,” using money to determine outcomes. We haven’t done enough fast enough because money hasn’t been used effectively to move the levers of corporate control. The Internet did not come to dominate the globe because of divestments from AT&T or protests in front of FCC offices. IBM didn’t come to dominate the computer industry for a generation because they were punished for their punch-card machines. Transformation requires investment, vision, and collaboration.

Consider the outcome of the world’s efforts so far: political backlash against “ESG Investing,” the head of a fossil fuel company leading the next COP, GM building gigantic trucks that still require excessive energy resources to power, and the petroleum industry dressing up every one of their websites with lovely green pictures.

In contrast, there are real groups, with real boots on the ground, engaging directly with fossil fuel companies and new energy market innovators to exert influence and drive change by direct financial and managerial involvement. While this approach leverages the market’s financial machinery, it is more direct and efficient than ESG investing.

ESG Investing

ESG Investing developed over decades to try to address social concerns about how companies operate. Partly because of the conversations and awareness generated by climate activism, demand arose for ways people could invest money and not feel bad about where their investment dollars were going.

It is a market-driven fund and portfolio management strategy with many different implementations. There are overlaps with INvestment strategies focused on putting money into “green” businesses, DIvestment strategies that sell stock to punish miscreant companies and, aspects of how funds vote in shareholder elections.

But the innovation of this noble-sounding branding of money management practices comes with multiple caveats. ESG problems include:

- Very noisy data about corporate behavior

- Lack of standard metrics and definitions

- Susceptibility to greenwashing

- It’s yet another front in the culture wars

- The same tactics can be used to further oppositional goals

Scores and metrics are used to supposedly summarize how a fund or stock aligns with shareholder desires but there is no uniformity, regulation, oversight, or history of best practices to define a disciplined methodology for calculating scores. ESG ranking is an immature industry filled with competing players jockeying for power and financial gain.

ESG investing is indirect, unregulated, and in many cases ineffective, very often primarily concerned with attracting money, which the funds charge to manage, rather than truly effecting change. Fund managers want investors to feel good, and invest in their products rather than those offered by a competing fund. Caveat emptor. The investor is left with the job of trying to analyze and vet the ESG claims of different funds – an impossible task for most.

For example, the widely used MSCI benchmark, discloses in its methodology document that its ESG rating only ranks the financial risk to a company and its investors with respect to environmental, social, and governance practices. In other words, it answers the question “If this company pumps a billion barrels of oil is there risk that its financial health will be negatively impacted, e.g. by a lawsuit or regulation? Will I lose money?”

Vanguard’s ESG disclaimer for their ESG-labeled funds is a shining example of the thesis that much of this is really a marketing play. It says, in part, “companies deemed eligible by the index provider or advisor may not reflect the beliefs and values of any particular investor and may not exhibit positive or favorable ESG characteristics.”

There is also existential risk that comes with ESG investing as with glossy activities like COP. Big Oil has received the message that they must at least appear green enough to get positive ESG rankings. They will work to create an image that just passes ESG muster at the lowest possible cost. For example, a company could use ESG rating as a pretext to chase money-grab investments in moonshot geoengineered adaptation, or as recently has been proposed, utilize captured CO2 under pressure to pump petroleum, and score points.

The culture wars have been playing out on the ESG battleground. Axios has reported several times on the active resistance from pro-oil interests and “conservative” stakeholders against ESG initiatives. According to this report “GOP committees are already planning to haul in the CEO’s of investment firms…for public lashings…” Another Axios report profiles Vivek Ramaswamy, who hopes to displace the large fund managers because of their ESG practices. He is actively wooing state officials to convince them to move asset management to his firm and wrest corporate voting power from the funds voting for progressive and climate-favoring action. Ramaswamy has backing from powerful GOP lawmakers.

For all this effort and angst, as is also true with divestment strategies, data doesn’t indicate that the ESG investing movement has altered the course of the fossil fuel industry. As with divestment, basic statistics such as oil production, greenhouse gas emissions, and financial returns of polluting companies demonstrate that so far there is nothing to show that ESG is working to change the trajectory of climate destruction.

Direct Engagement & Impact Investing – a Necessary Future

There is an alternative which does not get as much press and does not generate the agitation or attention that accompanies divestment and ESG themes.

A growing number of organizations are embracing the use of financial market investment mechanisms to engage directly with corporate decision makers. Money buys close contact with corporate boards and seats at the governance table. Sometimes called “impact investing” or “activist investing” their engagement strategies are based on core principles of market functioning and give these organizations an express lane to influence and change. A few are highlighted here.

As You Sow

As You Sow bills itself as “the nation’s non-profit leader in shareholder advocacy” and concisely articulates the thesis that active engagement is the best path to change:

“Corporations are responsible for most of the pressing social and environmental problems we face today — we believe corporations must be a willing part of the solutions. We make that happen. As shareholder advocates, we directly engage corporate CEOs, senior management, and institutional investors to change corporations from the inside out.”

They target an array of corporate responsibility issues, not just those related to climate destruction. This page discusses their energy and environment work, which includes the petrochemical sector as well. By introducing shareholder resolutions, and fighting legal battles against regressive attempts to throttle active corporate engagement, they are on the front lines of a fight to ensure that corporate behavior can be influenced by shareholder votes and that executives are held accountable for their policies. Their “Invest Your Values” page allows investors to drill into objective data from Fossil Free Funds and get clear metrics about fund involvement in polluting and misbehaving corporations.

As You Sow also hosts a page on how shareholder resolutions and voting work, an essential introduction to the mechanics. “Vote Your Values” is a program for connecting shareholders to proxy voting, similar to what large fund managers are starting to do as described in the next section on Blackrock.

Blackrock & Large Funds

Blackrock and other giant investment management companies such as Fidelity and Vanguard are also on the front lines of the fight for how corporate finance can be used to influence corporations and force strategic shifts. This is ground zero where the forces of divestment, ESG, and impact investing all detonate together because of the massive size of these funds.

Because they offer funds containing huge blocks of shares in multiple companies to investors, they have a significant say in the corporate resolutions submitted and outcomes of shareholder votes. With these group, or index, funds, investors participate in the financial gains and losses of a large selection of stocks but do not directly have shareholder rights. Instead, the fund managers vote the shares and have been increasingly more vocal in proposing and backing environmental policy changes.

Blackrock is working on changes to bring investors in their funds closer to the voting process, and reports “tremendous interest.” Vanguard has also just announced a similar effort. This is a more direct connection between the investor and voting outcomes which is positive for advocates of change but just as positive for advocates of status quo or increasing fossil fuel exploitation. These moves are also a response to the political pressure to diffuse the power of the fund managers, as mentioned above. It’s complicated in one sense but in another it’s simple: large numbers of investors, large and small, must enter the fray and cast their votes at shareholder meetings.

The Guardian just reported that Norway’s sovereign investment fund, the world’s largest, has made it clear to its portfolio companies’ board members that “it will vote against their re-election to the board if they do not up their game on tackling the climate crisis, human rights abuses and boardroom diversity.” With $1.2 trillion dollars under the fund’s control companies have to pay attention.

Engine No. 1

Engine No. 1 runs two funds that are specifically designed to work with companies to create change collaboratively.

This article tells the story of how Engine No. 1 won seats on the board of Exxon. After that expensive experience and shifting to a more cooperative engagement strategy, they were able to persuade ConocoPhillips and others to join the UN Oil & Gas Methane Partnership which is “the only comprehensive, measurement-based reporting framework for the oil and gas industry that improves the accuracy and transparency of methane emissions reporting in the oil and gas sector.”

Engine No. 1 offers investors commitments on how the funds’ proxy votes will be cast. This means that an investor in their funds participates in the investment returns and knows with assurance that the fund shares will be voted to either support Engine No. 1’s more general principles (“VOTE” fund) or specifically focus on environmental transformation (“NETZ” fund.) They emphasize that their goals are to create economic benefit by persuading companies to be responsive to demands for more progressive governance.

Because Engine No. 1 directly engages with the companies most in need of change, their third-party ESG ratings are low – another case where ESG investing shortchanges those seeking real change. Engine No. 1 holds positions in fossil fuel companies, but they do so specifically in order to buy those seats at the governance table, not as a side effect of building large diverse sector or index funds such as Blackrock’s or Vanguard’s.

The difference between Engine No. 1 and the large funds trying to vote their influence is that their strategy is laser focused and transparent, active, and pulling investment dollars directly into transformational change action at their portfolio companies.

There are few roadblocks or controversies following this strategy. Nothing stands in the way of this bee-line to fostering change within the core of corporations except the attainment of critical mass. Large numbers of investors selecting funds specifically focused on changing corporate behavior, rather than relying on vague and gameable ESG scores via the major fund managers, can effect real change.

The counterpoint, of course, is that there is nothing to stop pro-petroleum and regressive funds from following the same strategy, as Vivek Ramaswamy is doing. There will be no escaping the culture war entirely.

Follow This

Follow This provides an option that allows people who aren’t otherwise investors to buy a single share in an oil company, becoming a shareholder of record. With a large number of shares sold to a constituency demanding change, Follow This’ leaders have the same path to corporate decision makers as other fund managers. They have been filing shareholder resolutions at major oil companies since 2016 and the results of shareholder votes page shows the organization’s effectiveness.

Investors who already own shares in oil companies can join Follow This and have those shares counted along with the other supporters buying shares or donating money. This doesn’t constitute direct voting power but increases Follow This’ credibility and clout at the bargaining table. Investors would still have to cast their own ballot in the corporation meeting elections for their shares to count in official resolution vote tallies.

Follow This also reaches out to the giant fund managers and contributes input on resolutions. This is a more direct route to influencing fund managers than investors trying to vote their dollars via selecting loosely defined ESG funds, and it’s a path for people who don’t directly invest to exert influence they would not have otherwise. In 2022 Follow This wrote a letter directly to large fund managers to invite a collaboration on resolutions for 2023 corporate voting.

Challenges

Any attempt to change incumbents who do not want to change will face resistance. Direct engagement, shareholder advocacy and proxy voting all face challenges. Rules have recently been put into place to push back on activist shareholder resolutions at corporations’ annual meetings. Legislation has been introduced to inhibit large fund managers from voting the blocks of shares in their index funds, in a display of sudden and inexplicable interest in shareholder democracy. The same mechanisms of direct engagement are being put into place by pro-petroleum and regressive special interests.

There is no single magical market dynamic that will solve our problems of environmental destruction, but we are obligated to use the best and most powerful tools available to further our aims despite the challenges.

Use the Money: Summarizing Key Points

- Neither agitating for divestment nor vaguely defined and unaccountable ESG investing strategies have moved the needle when it comes to getting fossil fuel corporations to demonstrably change.

- The entire financial and political world, in response to the loud and clear message that the public wants change, is now in an escalating culture war with investment dollars as the primary weapon in the fight for control of corporate behavior.

- Divestment can be a useful strategy, if the right companies are targeted: smaller entities that are nevertheless in the critical path of larger and highly destructive projects and plans. Insurance companies, smaller banks, PR and accounting firms, and professional technical service companies might be influenced by divestment - whereas giant banks and oil companies view calls for divestment as political, PR and marketing annoyances.

- ESG investing is a noisy chaotic unregulated marketplace. There are investment funds marketing ESG to chase assets they manage for a fee, regulators and politicians trying to blunt its effectiveness, data brokers cooking their own sets of ESG ratings books and trying to sell them to the fund managers, lawyers making sure the fund managers have no liability or accountability when it comes to effecting real change, and targeted companies dressing up their websites and token project portfolios to get ESG points.

The good news is that there is a group of committed organizations focusing on the bullseye: active and direct involvement in multiple corporate governance processes. They focus investor dollars straight into the boardroom to exert pressure, persuade, and advocate for change. There is no need to march, throw eggs, get arrested, and go to jail; that mission has been accomplished, that part of the war is over, the streets and museums are no longer a useful battleground.

As You Sow, Engine No. 1 and Follow This can point directly to cases where their engagement was instrumental in effecting change at the highest levels of fossil fuel corporate management. And anyone can become a part of that process with a few clicks.

If everyone calling for divestment or parading in front of Wells Fargo bought a share of BP through Follow This for $13.00 instead, or if investors in Blackrock’s funds moved to Engine No. 1 or bought/pledged shares with Follow This it would send a signal almost as loud and clear as Musk buying Twitter: We Demand Change, Change is Coming.

Your Call to Action

Anyone and everyone can use investing as a powerful force for undoing the process of climate destruction.

If you do not participate directly in investing, weigh in through Follow This and buy a share which buys another vote for a survivable climate. If your 401K offers a selection of funds, investigate the fund using As You Sow’s independent and progressive scoring tools and use their retirement plan action page. If you are an investor, consider moving to Engine No. 1 from other broad index and ESG funds, or get involved in your fund manager’s proxy voting initiatives.

Attention needs to shift in very large numbers to the corporate boardroom and executive suite. Money must be mobilized as the tool of choice for fixing climate abuse. The market system is specifically engineered for purchasing corporate influence and control by investing in company stocks, and that is the mechanism that will create true transformation.

Fossil Fuels Divesting: Time for an Upgrade

Divestment has been a powerful symbolic statement, but a climate damage countermeasure? Not so much - it’s time to change the model.

Intro

We’re all here, and you are reading this, because we need the fossil fuels producing and consuming industries to change. Despite overwhelming consensus about the need, there is disagreement and uncertainty around how to force the change.

This three-part blog series is about using money as a powerful tool to move these industries away from their destructive practices. The first installment talked about the two levers of financial force: punish companies by divesting (directing money flows away from them) or investing (reward and support companies by directing money towards them.)

While the next article will talk about how activist, impact and ESG models are moving the investment lever, this installment will focus on what’s been happening in divestment and its impact, offer a guide for getting involved in a new generation of divestment actions.

Summary

There’s no question that the divestment movement has had a powerful impact in the fight to stop climate destruction: Many organizations, that collectively control an enormous amount of total assets, have announced support or implementation of divesting. The press reports widely on divestment and it is hotly debated at the highest levels. The divestment movement’s greatest achievement has been calling widespread attention to the potential role of finances in influencing the fossil fuel industry.

But along with all this attention there is churn, noise, recrimination, and backlash. There are significant issues with the numbers and statistics being used, and the charts below show that divestment has not resulted in decarbonization. There are problems with divestment as it is currently defined and manifested so it’s time to update our model of what works.

The state of the current divestment-as-climate-activism movement can be summarized in a few bullet points:

- The divestment movement that started during the last 5 to 10 years has made major contributions to the growth of ESG investing models and shifts in renewables investment.

- Despite that, there is no evidence of direct influence on fossil fuel production, or the finances of fossil fuel companies.

- There is credibility damage and misinformed debate because of how divestment numbers are being reported.

- Legislative backlash against divestment is growing as lawmakers and fossil fuel stakeholders retaliate against companies that are divesting.

- Backpedaling and apathy from large investors demonstrates they are unwilling to forgo profits.

- The current divestment environment is risking a prolonged stalemate that depletes attention and energy while the climate crisis continues unaffected.

But:

A new divestment model that I call “Divestment 2.0” matures divestment strategy, focusing less on fossil fuel companies themselves, and more on companies providing critical services that enable them.

These targets are more directly influenced by asset divestment because their bottom lines are not driven by commodity markets, they often have lower market caps and can be impacted more cost-effectively, and they have shareholders with different goals and risk appetites.

In a shift to Divestment 2.0 there is a larger selection of companies that can be removed from portfolios, impacting a broader swath of the infrastructure that powers fossil fuel companies. Insurance companies, brokers, banks, ratings agencies (Standard & Poor’s, Moody’s), and service providers of all types become candidates for divestment if they continue to enable destructive projects.

And shifting divestment strategy away from fossil fuel companies might make divestment less of a political target.

Most importantly, stopping the flow of services into fossil fuel companies directly inhibits them from continuing to do business and damage as usual. Focusing divestment on companies serving the fossil fuel industry rather than polluting companies themselves may be a more direct path to achieving the strategic goal.

Divestment 1.0 – The Current State

In the first article, I pointed out that divestment can refer to several ways of directing money away from a company to punish bad behavior. In addition to selling financial stakes such as shares of stocks, withholding lending and insurance support can be another. Boycotting, taxation, and other direct financial penalties also interfere with the flow of money into a company; however, this series will not go into those strategies.

Divestment - sales of fossil fuel companies’ stock - is of questionable benefit If the intention is to directly affect fossil fuel companies’ finances or inhibit their ability to do business. It is difficult, if not impossible, to connect stock price and market cap holdings with how companies behave: divestment data is unclear, missing, or misleading, and innumerable other factors besides stock prices control company strategy and action.

FUDging Stock Divestment Numbers

According to Stand.Earth’s Divestment Database “Approximately $40.57 trillion” (which I’m going just call $40T) is the “value of institutions divesting” from fossil fuels, with 1546 organizations listed. The list includes faith-based organizations, educational institutions, investment firms, endowments, pension funds, and governments that have said they have divested or will divest from the fossil fuel industry.

But the problem with that figure is that it doesn’t measure actual impact on fossil fuel companies or decarbonization, and it significantly overstates how much money is even potentially in play.

The divestment database tallies the total amount of money managed by all listed entities, not how much is relevant to investment in target companies. Of 1546 divesting organizations listed, many are also NGO’s that have no financial stake or stocks invested in fossil fuels companies. Their assets should not be counted in a tally of the “value of institutions divesting” at all. Wikipedia echoes the statistic circa 2021: “a total of 1,485 institutions representing $39.2 trillion in assets worldwide had begun or committed to a divestment from fossil fuels.”

Three examples show how reality differs from the impression created by that huge asset value number.

- The Catholic Church states they manage $14T in total assets across all their investments, so Stand.Earth reporting makes it seem as if $14T in assets are being divested from fossil fuels. Earthbeat, as many others do, repeats the statistic uncritically. However, the reality is that only a fraction of their total assets is invested in fossil fuels to begin with, according to this article from Reuters.

- Blackrock is a behemoth investment manager that has been widely touted as divesting from fossil fuels. It accounts for $8T assets under management (AUM) of the $40T amount that Stand.Earth reports. But only about 1% of their assets, roughly $93B, is in fossil fuel related investments.

- Two giant California pension funds, CalPERS and CalStrs have a combined asset base of $796B. Of that, only about $7.4B is invested in fossil fuel companies, about 1% of assets under management.

Saying that $40T has been divested from fossil fuel projects or companies creates a credibility gap – it is meaningless and misleads people into either wondering “what did we actually accomplish with all that divestment?” or believing we’ve turned the corner because “look how much money is being divested!” This gets in the way of being effective and achieving our goals. It demonstrates that a different approach to divestment strategy is needed, one that is more achievable and measurable.

Earth.Stand did not respond to my questions about the database and whether there is any data on actual divestment dollars directly moved away from fossil fuels companies, or the justification for using total assets managed as a benchmark.

Direct Impact of Divestment 1.0

Not only is there confusion and conflict around the divestment movement, but it hasn’t demonstrated any effects on the production of more greenhouse gas pollution.

These graphs below show the disconnect between divestment and fossil fuel company behavior, given that divestment assertions have been growing steadily since about 2014.

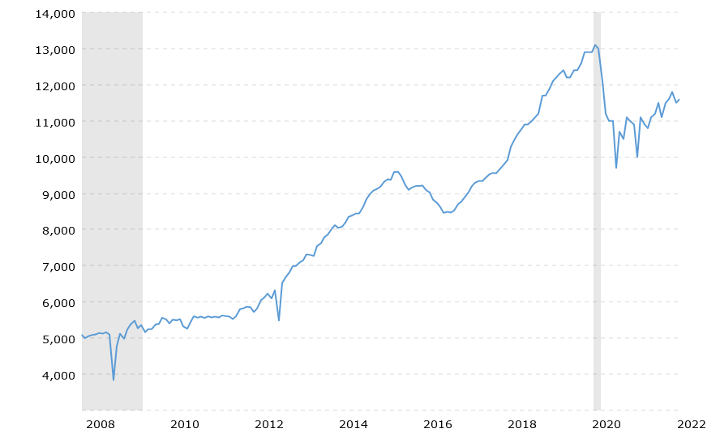

United States oil production

U.S. Crude Oil Production - Historical Chart

The production of oil in the US has been increasing dramatically since the 2008 financial crisis. The drop in 2020 is the result of the pandemic but has been recovering roughly along the trend line.

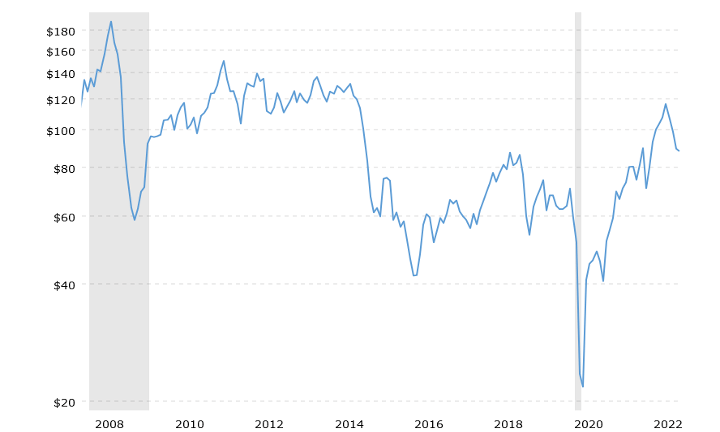

Oil prices and company income/earnings

The commodity and supply/demand relationship effect on company earnings is shown in the next graphs:

Earnings are a direct reflection of oil prices, and earnings are by far the most significant measure of a company’s success, as opposed to share price:

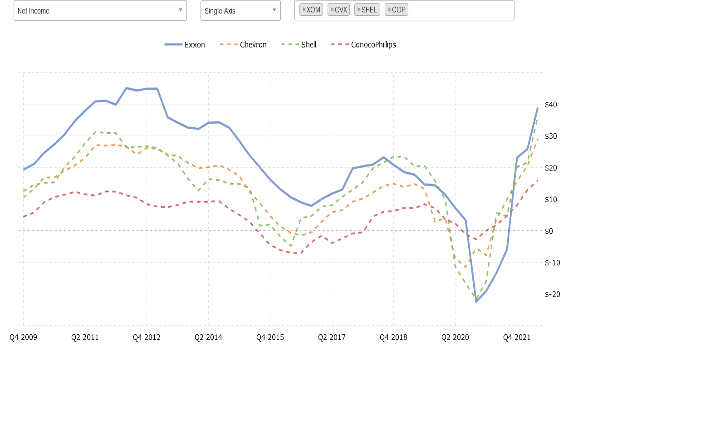

Net Income for 4 Largest US Co’s

Stock prices

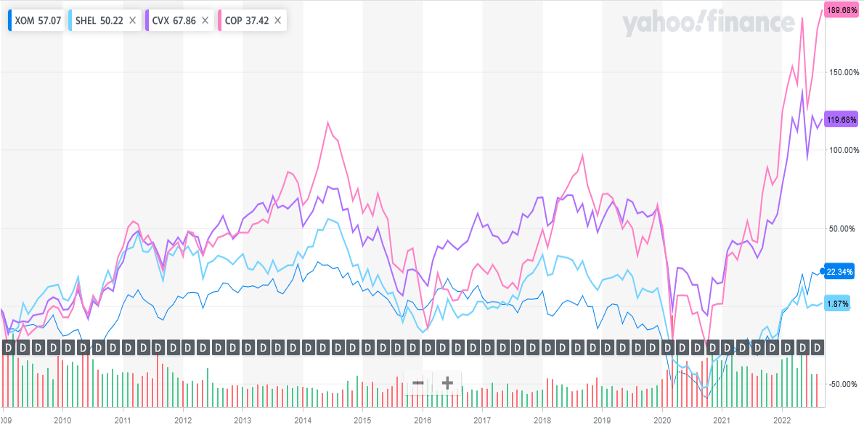

And here are stock prices for four major oil companies, where you would see the divestment effect if it existed. But these graphs correlate with the charts above that show the effects of supply and demand on earnings, and no correlation with the growth of divestment pledges. Stocks move in response to the bottom line.

Stock Price for 4 Largest US Oil Co’s

Has Divestment 1.0 Helped?

So there have been no reduction of fossil fuel production, or any stock price or volume changes showing massive numbers of shares traded due to divestment. The driver for the stock price declines is the decline in sales and profit, and that decline is driven by the decline in oil prices, and that is driven by “the market” and commodity supply/demand. The metrics don’t support a claim that the divestment movement has resulted in benefit to the environment such as reducing the amount of oil production or changing fossil fuel company behavior.

Fossil-fuel-stock-sales-based Divestment 1.0 has also created a culture war and opened a new front in the climate struggle. The divestment battle grabs attention, escalates hostilities, and sparks conflict between financial managers and regulators, but we’ll see that the Divestment 2.0 model has the potential to mitigate this.

Meanwhile, the charts speak for themselves – the greenhouse gas crisis has continued to worsen because of forces at work that have nothing to do with trading shares in fossil fuel companies.

The Divestment Movement’s Greatest Success

On the positive side, there is no question that the messaging around divestment has contributed to forcing important changes and new discussions, even if it has not had a direct financial or decarbonization impact.

A global scale, resounding, and important message was added to the climate debate when the divestment movement started. The message was “we are going after the money,” and that is a powerful message for us to send. The strongest positive result of the movement to date has been forcing these other conversations to happen.

For years, the divestment theme has helped drive the creation of the ESG (Environmental, Social, Governance) investing movement, the subject of the final article in the series.

I think that part of the mission has been accomplished.

What’s Next? Divestment 2.0

It’s time to mature and evolve the divestment movement, shifting its focus. There are other paths to change that asset managers and individuals can leverage instead, and to better effect – what I term “Divestment 2.0.” This means a greater focus on the other financial flows and services that have a direct impact on fossil fuel company profits and ability to do business.

The shift to divesting from financial institutions funding fossil fuels projects, services sectors such as accounting & auditing firms, consultants, or even IT providers can be more effective than divesting from the fossil fuel companies themselves because:

- They may be more affected by divestors taking their business elsewhere.

- They may be more affected by changes in stock price and reputation.

- Their earnings are not directly affected by commodity pricing and demand.

- They are sometimes smaller companies that can be influenced more efficiently.

If banks are pressured to refuse lending to fossil fuel projects because fund managers see outsized risk in the investments, the projects cannot proceed.

If insurance companies are pressured to refuse to insure fossil fuel projects because fund managers deem the risk to its shareholders as unacceptable, the projects cannot proceed.

And so forth.

Without new projects, fuels production doesn’t expand, supply gets depleted, price goes up, and other technologies step up to provide better solutions, as is already happening. This creates a multiplier effect and is a more direct, visible, and powerful lever than indirect methods of selling fossil fuel company stock. This is the strategy that “Divestment 2.0” should employ at global scale. This is the “free market” – a system that conservatives and lawmakers are supposed to understand.

Risk Management

One of the most important benefits of the shift to Divestment 2.0 is that it emphasizes divestment as risk management in the best interests of investors. This reframes divestment as protecting the investor class from risk, which resonates from Main Street to Wall Street and should be understood across political boundaries.

Evidence-Based Divestment Metrics

This approach also allows hard clear evidence of divestment effects to be seen, eliminating FUDging and handwaving. The pressure on financial services companies results in withholding of funding to fossil fuels companies which results in stopped projects. The size and scope of abandoned projects and strategic shifts – changes in capital investment patterns, for example - can be quantified.

Case Study: EACOP - Insurance Companies & Banks

For example, the East African Crude Oil Pipeline is a giant project that would run a heated pipeline hundreds of miles and disrupt massive ecosystems to deliver 2.2B barrels of oil. From Wikipedia:

“The East African Crude Oil Pipeline (EACOP), also known as the Uganda–Tanzania Crude Oil Pipeline (UTCOP),[3][4] is under construction[5] and intended to transport crude oil from Uganda's oil fields to the Port of Tanga, Tanzania on the Indian Ocean.[6] Once completed, the pipeline will be the longest heated crude oil pipeline in the world.[7] Because of the large scale displacement of communities and wildlife, global environmental groups are protesting its construction and finance.[8][9]”

Stop EACOP, 350.org and others have been driving a vigorous campaign to go after the sources of funding and insurance for the project.

This is the future - Divestment 2.0, as being implemented by Stop EACOP’s Go Global campaign. Quoting their website:

“STOP THE FLOW OF CORPORATE MONEY

If completed, the East African Crude Oil Pipeline will displace communities, endanger wildlife and tip the world closer to full-blown climate catastrophe. We need to #StopEACOP.

Building the biggest heated oil pipeline in the world is expensive work and Total and China National Offshore Oil Corporation can’t go it alone – they need support from investors, banks, insurers, technical advisors and construction contractors from around the world.

That’s where you come in!

We know from experience that companies take notice when enough people speak up about their decisions and actions. For example, following our advocacy, the African Development Bank has declared it is not financing the pipeline. So who’s next?

If we can stop the money pipeline to EACOP, then we can stop the actual pipeline.”

The African Development Bank isn’t the only successful Divestment 2.0 outcome, per these reports:

Eacop’s financing blues as lenders desert $3.5b project

Insurers refusing to secure EACOP

Banks that are in, or out on EACOP

Global PR Firm Reportedly Cuts Ties With Bank Over African Oil Project

Divestment 2.0 Fights Need Your Support

The battle is ongoing. Giant insurance broker and risk manager, Marsh McLennan, (stock symbol MMC) is the focus of an intense skirmish as they have signed on as the “insurance arranger” for EACOP. 350.org is sponsoring a campaign against Marsh because without Marsh McLennan there may be a good chance to stop EACOP.

Here is how you can start your commitment to Divestment 2.0:

If you are an investor

- Check your portfolio for ETFs holding MMC (or check your mutual fund) – ETFs hold a combined total of 43M shares, about 9% of MMC’s market cap.

- Find replacement ETFs without MMC holdings.

- Contact your advisor and discuss how to remove MMC from your portfolio

- Make sure to send a letter to MMC telling them of your divestment

- Promote your divestment on social media

And for everyone, become part of the conversation on social media and via 350.org’s campaign and reach out to other divestment campaigns to urge adding companies in the financial supply chain to their lists of divestment targets.

Another organization to reach out to, Extinction Rebellion Bay Area, staged an action at Chase Bank in San Francisco to call attention to the financial giant’s funding of climate-destroying projects. (Although the size of Chase makes it a daunting target, its business model relies on risk management, and it can be affected by more and different factors than the oil majors.)

These sorts of actions should be on your “short list” of ways to get involved and have an impact.

Next Up: Investing and ESG

In the next and final segment of this three-part series, I will talk about the other side of the divestment coin, which is INvestment - the other financial lever we can use to change behaviors. And I’ll give you as concrete example of how I personally have used investment to support the battle against EACOP.

If precision INvestment strategies can get as much traction as DIvestment and ESG, multiplier effects will continue to compound the effectiveness of exercising financial power. See you there!

If you have made it this far, I want to sincerely thank you as I feel personally passionate about effectively wielding financial power in the fight for the climate.

I hope that readers come away with new appreciation for the need to expand our definition of divestment and update divestment programs to reflect lessons learned. This can help individuals make better decisions about supporting organizations or how to manage their own assets.

Climate Collapse? Money Talks.

Investing and divesting as tools for mitigating climate destruction

We know all the cliches: Money talks, BS walks. Money makes the world go round. Put your money where your mouth is. Follow the money. Yes, cliches are overused and trite, but that’s because they capture an essential truth. The simple truth is that in the campaign for a livable climate and mitigating climate destruction, money is key.

For better or worse, barring mobilization of vast numbers of people to confront climate destroyers via in-person direct action, using money is going to be how we win the battle for a livable climate and secure future.

This is the first of three articles looking at how financial impacts can be used to motivate change in climate-impacting companies:

- First, a look at how investing and divesting can influence corporate behavior

- Then, analyzing successes and failures resulting from investing and divesting approaches

- Lastly, “ESG” (Environmental, Societal, Governance) investing themes are evolving to help motivate change

Money is Leverage

In this first article, I’ll review the two financial levers with the capacity to move the massive weight of corporate dominance over climate health: investment and divestment.

Corporations know only one simple fact when all the complexity is reduced to fundamentals: money is either flowing IN to and enriching them, or money is flowing OUT and away from them and reducing their value. By controlling the flow of dollars into and out of corporations, they can be influenced. It’s that “simple.”

Here I’ll briefly discuss how ownership or sale of large blocks of stock, and banking and lending policies, can impact and shape corporate climate behavior. There are only two choices: Invest in and support a company financially to influence how it operates, or Divest from and remove support, at scale, to punish bad behavior, send a message, or make a personal statement. How does this work?

How Investing Practices Can Influence Corporate Behavior: A Primer

Shareholder Rights

The most important aspect of investing as a tool to influence corporate behavior is this:

“Perhaps one of the most important principles of corporate governance is the recognition of shareholders”

“The policy of allowing shareholders to elect a board of directors is critical. The board’s “prime directive” is to be always seeking the best interests of shareholders”

This is the fulcrum of the investment lever to promote corporate change: the shareholders own the company, they elect the board of directors, and the board of directors is mandated to put executives and mechanisms in place to serve the interests of the shareholders.

“This means that shareholders, effectively, have a direct say in how a company is run.”

Also, shareholders want to maximize the influence of their stake in a company, so they are motivated to reach out to current or prospective customers, government, or other external participants, to influence them to do what’s in their, the shareholders’, best interest. This is a “force multiplier” that reaches beyond the boardroom.

(See https://corporatefinanceinstitute.com/resources/knowledge/other/corporate-governance/)

Shareholders have additional rights to protect their self-interest, beyond voting on resolutions and board members:

“Opportunity to inspect corporate books and records. Shareholders have the right to examine basic documents such as company bylaws and minutes of board meetings. In addition, the Securities and Exchange Act of 1934 requires public companies to periodically disclose financials.

The right to sue for wrongful acts. Suing a company typically takes the form of a shareholder class-action lawsuit.”

(See https://www.investopedia.com/investing/know-your-shareholder-rights/)

Proxy Voting

Each year, companies hold a shareholders’ meeting in which governance issues are voted on. In preparation, relevant information is provided to the shareholders: financial reports, shareholder resolutions, executive compensation levels, and board member nominations. At the time of the meeting, shareholders can vote on governance matters directly, or via a proxy mechanism where they delegate their vote to an investment manager, hedge fund, company management, or other intermediary.

(See https://www.investopedia.com/terms/p/proxy-vote.asp)

This voting power gives holders of large blocks of stock a significant say in how a company is run, and how it is held accountable, or not, for behaving appropriately. If most of a large fund’s investors defer their vote to their fund manager by proxy (which is typical,) the vote from the fund could have major impact.

Even if a fund doesn’t have a large block of shares, it can still present resolutions for a shareholder vote, which also can be significant leverage.

Incumbent interests don’t want “activist” shareholders showing up and causing disruption over changes in company strategy. In response to this threat, legislation is being discussed that would limit the ability of large index funds to vote their very significant blocks of shares, to shield companies from progressive action being taken by the funds. Senator Dan Sullivan (R-Alaska) has introduced the “INDEX” bill that would stop giant investment funds like Blackrock and Vanguard from directly using shares they hold on behalf of their customers to force companies into doing more to mitigate their climate damage.

In contrast to the various tools available to shareholders to affect company behavior, non-shareholders must rely on extrinsic forces to shape corporate actions. There are two primary means to do this: political involvement to influence regulation and legislation, and public pressure such as protest and boycott. These approaches have their own advantages and challenges, and have their place, but are at arm’s length from effecting change within companies.

Influence of Lending

Another mechanism for financial engagement with a company is to lend it funds. All large companies are in some way reliant on debt financing to operate, and the large amounts of money involved mean there are deep legal and operational ties between company and lender. Having the decision-making power whether to make a loan and under what terms gives the lender a mechanism for shaping the borrower’s behavior.

Commercial banks who use the public’s deposits for capital to invest can potentially be influenced to apply financial leverage in negotiations with prospective borrowers, putting conditions in place that reflect the will of the public. ESG Lending refers to setting loan terms that are tied to sustainability and other “social good” performance metrics, reflecting both public and financial industry pressure. Banks’ desire to both cultivate a positive image and satisfy regulatory risk management requirements contribute to the growing attention on “sustainable lending.”

(See https://www.jdsupra.com/legalnews/esg-loans-the-next-big-wave-in-fund-6869513, https://www.lsta.org/news-resources/what-is-esg-linked-lending-and-why-do-we-care — there are many internet sources on this topic)

How Divestment Works

Divestment is the term for selling off shares in a company and disengaging from it. Divesting could also mean refusing to issue or renew loans, and possibly accelerating existing loans. Once fully divested, there is no more connection between the divestor and the actions, profits, or losses of the company.

Divestment of large amounts of stock impacts a company primarily through lowering its stock price, drawing attention to the company’s behavior, affecting perception of the company by the public and the market, and adding risk which influences lenders and investors.

If a large block of stock is sold off quickly, the share price is likely to drop at least temporarily. Executive compensation as well as personal net worth are based significantly on share price, so a large enough drop in price for a sustained period could get the attention of the company executives and board. There could be a reaction from the market that exacerbates the share price drop, as perception turns negative, news gets around, and a crowd starts to follow the selling trend. All this is a strong social signal with potential to change behavior.

There may be a significant enough move in stock price, or in sentiment, to alert lenders that the company presents a higher risk as a borrower. This could result in increased interest rates with a corresponding impact on the bottom line and add to a company’s negative outlook.

(See https://fairholder.org/blog/how-divestment-works)

The effectiveness of divestment continues to be debated, largely because as a “negative action” it’s difficult to connect the dots between a divestment decision and a change in corporate behavior. However, there is wide agreement that divestment sends powerful signals and makes a statement. The next article in this series will examine this issue in depth to look more closely for cause-and-effect.

As with activist investing, the divestment movement has caught the attention of pro-fossil-fuels interests and they are starting to fight back. This is a clear indication that divestment has an impact that is felt. For example, West Virginia has banned Blackrock, a huge investment firm, from doing business with the state.

Up Next: What Is Effective?

The fossil fuel incumbents’ negative reaction to the use of financial leverage to influence climate policy shows that it has an impact, whether the lever is investment or divestment. As I say at the start of the blog money talks, and when it talks, people listen — they don’t have a choice.

After this rudimentary outline of how investing in and divesting from publicly owned companies might influence companies, the next blog will look at the organizations using these different approaches and what results have been achieved. With an objective evidence-based analysis of what tactics are producing favorable outcomes, organizations can make decisions around what initiatives they can support or propose, and we’ll be taking a deep dive into pension fund, hedge fund, and grass roots movements’ effectiveness to see what is happening out there.

After that: ESG

Evolving patterns of activist investing and divesting at scale involves large legal and cultural shifts, most visibly the rise of “ESG Investing.” There is intense activity in this space with involvement of giants in regulation, technology, corporate governance, and public relations. This explosion of interest and visibility has brought with it confusion, competition, progress, deception, and political intrigue that will be the subject of a third part in this series of blogs. ESG metrics will play a critical role in both investment and divestment decision-making so it is an essential part of the analysis.

Disclaimer: this article is necessarily a very simplified description of an extremely complex field. It’s intended as a primer for those with little or no experience in how corporate finance is structured.

California Utilities Try to Destroy the State’s Rooftop Solar Progress

On behalf of three major investor-owned utilities, the California Public Utilities Commission has created a false premise to justify creating new rules that would gut rooftop solar incentives and penalize feeding owner-generated power back to the grid.

"NEM3" - Solar Nemesis

The California Public Utilities Commission (CPUC) is planning to issue rules that would penalize owners of rooftop solar panels for feeding power back into the grid, a process known as Net Metering. If these rules, called “NEM3,” are approved they will decimate forward progress on deploying distributed renewable energy, and punish homeowners and businesses for installing solar and wind power. This move will benefit only the investor-owned utility companies’ bottom lines and centralized business models, upon which their executive incentives depend.

The CPUC commissioned an elaborate “Lookback Study,” which they say justifies this move, but the study is incomplete and its methods susceptible to bias. The study, which was created by consulting firm Verdant Associates under the CPUC’s direction, guidance, and funding, leaves out critical measurements and had no outside vetting before it was used to drive the CPUC’s punitive proposal.

E3 Consulting, a firm specializing in energy utility operational research, used the Lookback Study results to create what is euphemistically called a “glide path” plan for enacting the NEM3 rules to achieve the utilities’ goals. Since the Verdant Lookback Study cannot be relied on due to serious validity concerns, the entire E3 “glide path” must be considered invalid. A new study must be done that addresses the failures of the current work, and a new proposal generated using complete and objectively verified data.

Otherwise, as they stand, the CPUC’s proposed rules would reverse the progress made on California’s distributed clean energy, when aggressive expansion and support to combat the climate crisis is getting more and more urgent.

Negative Impacts of NEM3 on Solar Adoption

Opposition to the proposed NEM3 rules needs to be vigorous since the negative effects on solar adoption are projected to be devastating.

The Sierra Club told the CPUC that the rules would “’crush the California rooftop solar market’ and its critical role in meeting the state’s climate objectives, improving local resiliency and reliability, and preserving our open spaces.”

California Solar & Storage Association writes “the proposed decision would impose large new fees on California families. These fees would be the highest in the nation, adding up to more than $600 per year. The proposed decision would also reduce the value of solar electricity sent back to the grid on hot summer days by 80%” (https://calssa.org/blog/2022/1/4/cpucs-proposed-nem-3-decision-would-hurt-solar-adoption-among-low-income-consumers)