Divestment has been a powerful symbolic statement, but a climate damage countermeasure? Not so much – it’s time to change the model.

Intro

We’re all here, and you are reading this, because we need the fossil fuels producing and consuming industries to change. Despite overwhelming consensus about the need, there is disagreement and uncertainty around how to force the change.

This three-part blog series is about using money as a powerful tool to move these industries away from their destructive practices. The first installment talked about the two levers of financial force: punish companies by divesting (directing money flows away from them) or investing (reward and support companies by directing money towards them.)

While the next article will talk about how activist, impact and ESG models are moving the investment lever, this installment will focus on what’s been happening in divestment and its impact, offer a guide for getting involved in a new generation of divestment actions.

Summary

There’s no question that the divestment movement has had a powerful impact in the fight to stop climate destruction: Many organizations, that collectively control an enormous amount of total assets, have announced support or implementation of divesting. The press reports widely on divestment and it is hotly debated at the highest levels. The divestment movement’s greatest achievement has been calling widespread attention to the potential role of finances in influencing the fossil fuel industry.

But along with all this attention there is churn, noise, recrimination, and backlash. There are significant issues with the numbers and statistics being used, and the charts below show that divestment has not resulted in decarbonization. There are problems with divestment as it is currently defined and manifested so it’s time to update our model of what works.

The state of the current divestment-as-climate-activism movement can be summarized in a few bullet points:

- The divestment movement that started during the last 5 to 10 years has made major contributions to the growth of ESG investing models and shifts in renewables investment.

- Despite that, there is no evidence of direct influence on fossil fuel production, or the finances of fossil fuel companies.

- There is credibility damage and misinformed debate because of how divestment numbers are being reported.

- Legislative backlash against divestment is growing as lawmakers and fossil fuel stakeholders retaliate against companies that are divesting.

- Backpedaling and apathy from large investors demonstrates they are unwilling to forgo profits.

- The current divestment environment is risking a prolonged stalemate that depletes attention and energy while the climate crisis continues unaffected.

But:

A new divestment model that I call “Divestment 2.0” matures divestment strategy, focusing less on fossil fuel companies themselves, and more on companies providing critical services that enable them.

These targets are more directly influenced by asset divestment because their bottom lines are not driven by commodity markets, they often have lower market caps and can be impacted more cost-effectively, and they have shareholders with different goals and risk appetites.

In a shift to Divestment 2.0 there is a larger selection of companies that can be removed from portfolios, impacting a broader swath of the infrastructure that powers fossil fuel companies. Insurance companies, brokers, banks, ratings agencies (Standard & Poor’s, Moody’s), and service providers of all types become candidates for divestment if they continue to enable destructive projects.

And shifting divestment strategy away from fossil fuel companies might make divestment less of a political target.

Most importantly, stopping the flow of services into fossil fuel companies directly inhibits them from continuing to do business and damage as usual. Focusing divestment on companies serving the fossil fuel industry rather than polluting companies themselves may be a more direct path to achieving the strategic goal.

Divestment 1.0 – The Current State

In the first article, I pointed out that divestment can refer to several ways of directing money away from a company to punish bad behavior. In addition to selling financial stakes such as shares of stocks, withholding lending and insurance support can be another. Boycotting, taxation, and other direct financial penalties also interfere with the flow of money into a company; however, this series will not go into those strategies.

Divestment – sales of fossil fuel companies’ stock – is of questionable benefit If the intention is to directly affect fossil fuel companies’ finances or inhibit their ability to do business. It is difficult, if not impossible, to connect stock price and market cap holdings with how companies behave: divestment data is unclear, missing, or misleading, and innumerable other factors besides stock prices control company strategy and action.

FUDging Stock Divestment Numbers

According to Stand.Earth’s Divestment Database “Approximately $40.57 trillion” (which I’m going just call $40T) is the “value of institutions divesting” from fossil fuels, with 1546 organizations listed. The list includes faith-based organizations, educational institutions, investment firms, endowments, pension funds, and governments that have said they have divested or will divest from the fossil fuel industry.

But the problem with that figure is that it doesn’t measure actual impact on fossil fuel companies or decarbonization, and it significantly overstates how much money is even potentially in play.

The divestment database tallies the total amount of money managed by all listed entities, not how much is relevant to investment in target companies. Of 1546 divesting organizations listed, many are also NGO’s that have no financial stake or stocks invested in fossil fuels companies. Their assets should not be counted in a tally of the “value of institutions divesting” at all. Wikipedia echoes the statistic circa 2021: “a total of 1,485 institutions representing $39.2 trillion in assets worldwide had begun or committed to a divestment from fossil fuels.”

Three examples show how reality differs from the impression created by that huge asset value number.

- The Catholic Church states they manage $14T in total assets across all their investments, so Stand.Earth reporting makes it seem as if $14T in assets are being divested from fossil fuels. Earthbeat, as many others do, repeats the statistic uncritically. However, the reality is that only a fraction of their total assets is invested in fossil fuels to begin with, according to this article from Reuters.

- Blackrock is a behemoth investment manager that has been widely touted as divesting from fossil fuels. It accounts for $8T assets under management (AUM) of the $40T amount that Stand.Earth reports. But only about 1% of their assets, roughly $93B, is in fossil fuel related investments.

- Two giant California pension funds, CalPERS and CalStrs have a combined asset base of $796B. Of that, only about $7.4B is invested in fossil fuel companies, about 1% of assets under management.

Saying that $40T has been divested from fossil fuel projects or companies creates a credibility gap – it is meaningless and misleads people into either wondering “what did we actually accomplish with all that divestment?” or believing we’ve turned the corner because “look how much money is being divested!” This gets in the way of being effective and achieving our goals. It demonstrates that a different approach to divestment strategy is needed, one that is more achievable and measurable.

Earth.Stand did not respond to my questions about the database and whether there is any data on actual divestment dollars directly moved away from fossil fuels companies, or the justification for using total assets managed as a benchmark.

Direct Impact of Divestment 1.0

Not only is there confusion and conflict around the divestment movement, but it hasn’t demonstrated any effects on the production of more greenhouse gas pollution.

These graphs below show the disconnect between divestment and fossil fuel company behavior, given that divestment assertions have been growing steadily since about 2014.

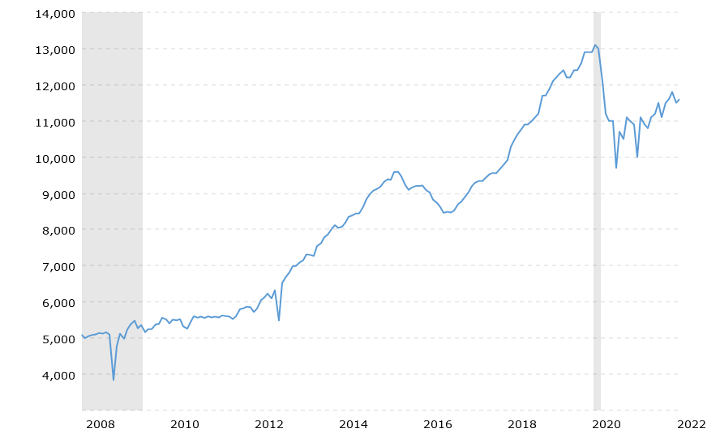

United States oil production

U.S. Crude Oil Production – Historical Chart

The production of oil in the US has been increasing dramatically since the 2008 financial crisis. The drop in 2020 is the result of the pandemic but has been recovering roughly along the trend line.

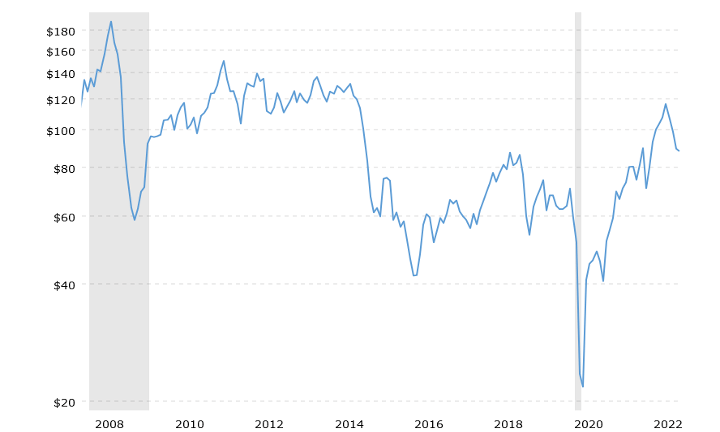

Oil prices and company income/earnings

The commodity and supply/demand relationship effect on company earnings is shown in the next graphs:

Earnings are a direct reflection of oil prices, and earnings are by far the most significant measure of a company’s success, as opposed to share price:

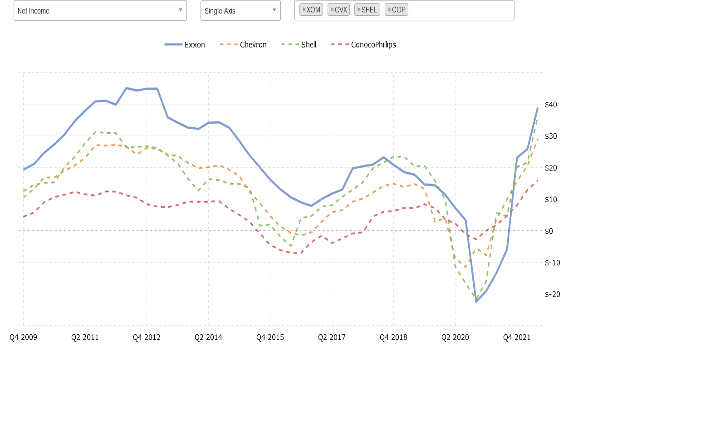

Net Income for 4 Largest US Co’s

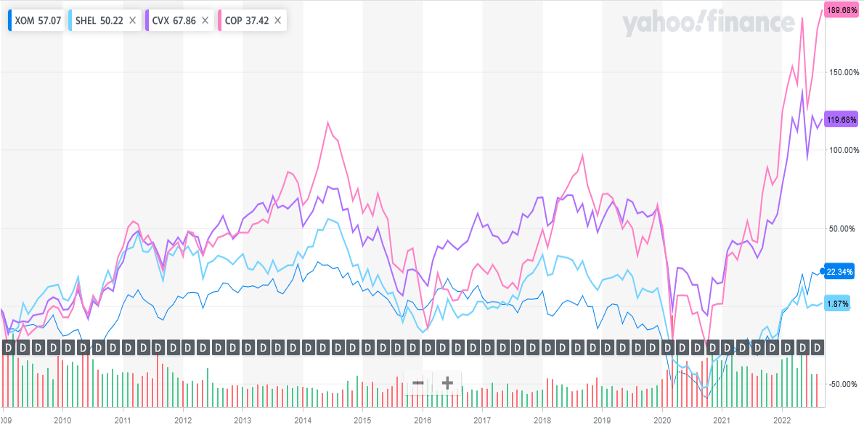

Stock prices

And here are stock prices for four major oil companies, where you would see the divestment effect if it existed. But these graphs correlate with the charts above that show the effects of supply and demand on earnings, and no correlation with the growth of divestment pledges. Stocks move in response to the bottom line.

Stock Price for 4 Largest US Oil Co’s

Has Divestment 1.0 Helped?

So there have been no reduction of fossil fuel production, or any stock price or volume changes showing massive numbers of shares traded due to divestment. The driver for the stock price declines is the decline in sales and profit, and that decline is driven by the decline in oil prices, and that is driven by “the market” and commodity supply/demand. The metrics don’t support a claim that the divestment movement has resulted in benefit to the environment such as reducing the amount of oil production or changing fossil fuel company behavior.

Fossil-fuel-stock-sales-based Divestment 1.0 has also created a culture war and opened a new front in the climate struggle. The divestment battle grabs attention, escalates hostilities, and sparks conflict between financial managers and regulators, but we’ll see that the Divestment 2.0 model has the potential to mitigate this.

Meanwhile, the charts speak for themselves – the greenhouse gas crisis has continued to worsen because of forces at work that have nothing to do with trading shares in fossil fuel companies.

The Divestment Movement’s Greatest Success

On the positive side, there is no question that the messaging around divestment has contributed to forcing important changes and new discussions, even if it has not had a direct financial or decarbonization impact.

A global scale, resounding, and important message was added to the climate debate when the divestment movement started. The message was “we are going after the money,” and that is a powerful message for us to send. The strongest positive result of the movement to date has been forcing these other conversations to happen.

For years, the divestment theme has helped drive the creation of the ESG (Environmental, Social, Governance) investing movement, the subject of the final article in the series.

I think that part of the mission has been accomplished.

What’s Next? Divestment 2.0

It’s time to mature and evolve the divestment movement, shifting its focus. There are other paths to change that asset managers and individuals can leverage instead, and to better effect – what I term “Divestment 2.0.” This means a greater focus on the other financial flows and services that have a direct impact on fossil fuel company profits and ability to do business.

The shift to divesting from financial institutions funding fossil fuels projects, services sectors such as accounting & auditing firms, consultants, or even IT providers can be more effective than divesting from the fossil fuel companies themselves because:

- They may be more affected by divestors taking their business elsewhere.

- They may be more affected by changes in stock price and reputation.

- Their earnings are not directly affected by commodity pricing and demand.

- They are sometimes smaller companies that can be influenced more efficiently.

If banks are pressured to refuse lending to fossil fuel projects because fund managers see outsized risk in the investments, the projects cannot proceed.

If insurance companies are pressured to refuse to insure fossil fuel projects because fund managers deem the risk to its shareholders as unacceptable, the projects cannot proceed.

And so forth.

Without new projects, fuels production doesn’t expand, supply gets depleted, price goes up, and other technologies step up to provide better solutions, as is already happening. This creates a multiplier effect and is a more direct, visible, and powerful lever than indirect methods of selling fossil fuel company stock. This is the strategy that “Divestment 2.0” should employ at global scale. This is the “free market” – a system that conservatives and lawmakers are supposed to understand.

Risk Management

One of the most important benefits of the shift to Divestment 2.0 is that it emphasizes divestment as risk management in the best interests of investors. This reframes divestment as protecting the investor class from risk, which resonates from Main Street to Wall Street and should be understood across political boundaries.

Evidence-Based Divestment Metrics

This approach also allows hard clear evidence of divestment effects to be seen, eliminating FUDging and handwaving. The pressure on financial services companies results in withholding of funding to fossil fuels companies which results in stopped projects. The size and scope of abandoned projects and strategic shifts – changes in capital investment patterns, for example – can be quantified.

Case Study: EACOP – Insurance Companies & Banks

For example, the East African Crude Oil Pipeline is a giant project that would run a heated pipeline hundreds of miles and disrupt massive ecosystems to deliver 2.2B barrels of oil. From Wikipedia:

“The East African Crude Oil Pipeline (EACOP), also known as the Uganda–Tanzania Crude Oil Pipeline (UTCOP),[3][4] is under construction[5] and intended to transport crude oil from Uganda’s oil fields to the Port of Tanga, Tanzania on the Indian Ocean.[6] Once completed, the pipeline will be the longest heated crude oil pipeline in the world.[7] Because of the large scale displacement of communities and wildlife, global environmental groups are protesting its construction and finance.[8][9]”

Stop EACOP, 350.org and others have been driving a vigorous campaign to go after the sources of funding and insurance for the project.

This is the future – Divestment 2.0, as being implemented by Stop EACOP’s Go Global campaign. Quoting their website:

“STOP THE FLOW OF CORPORATE MONEY

If completed, the East African Crude Oil Pipeline will displace communities, endanger wildlife and tip the world closer to full-blown climate catastrophe. We need to #StopEACOP.

Building the biggest heated oil pipeline in the world is expensive work and Total and China National Offshore Oil Corporation can’t go it alone – they need support from investors, banks, insurers, technical advisors and construction contractors from around the world.

That’s where you come in!

We know from experience that companies take notice when enough people speak up about their decisions and actions. For example, following our advocacy, the African Development Bank has declared it is not financing the pipeline. So who’s next?

If we can stop the money pipeline to EACOP, then we can stop the actual pipeline.”

The African Development Bank isn’t the only successful Divestment 2.0 outcome, per these reports:

Eacop’s financing blues as lenders desert $3.5b project

Insurers refusing to secure EACOP

Banks that are in, or out on EACOP

Global PR Firm Reportedly Cuts Ties With Bank Over African Oil Project

Divestment 2.0 Fights Need Your Support

The battle is ongoing. Giant insurance broker and risk manager, Marsh McLennan, (stock symbol MMC) is the focus of an intense skirmish as they have signed on as the “insurance arranger” for EACOP. 350.org is sponsoring a campaign against Marsh because without Marsh McLennan there may be a good chance to stop EACOP.

Here is how you can start your commitment to Divestment 2.0:

If you are an investor

- Check your portfolio for ETFs holding MMC (or check your mutual fund) – ETFs hold a combined total of 43M shares, about 9% of MMC’s market cap.

- Find replacement ETFs without MMC holdings.

- Contact your advisor and discuss how to remove MMC from your portfolio

- Make sure to send a letter to MMC telling them of your divestment

- Promote your divestment on social media

And for everyone, become part of the conversation on social media and via 350.org’s campaign and reach out to other divestment campaigns to urge adding companies in the financial supply chain to their lists of divestment targets.

Another organization to reach out to, Extinction Rebellion Bay Area, staged an action at Chase Bank in San Francisco to call attention to the financial giant’s funding of climate-destroying projects. (Although the size of Chase makes it a daunting target, its business model relies on risk management, and it can be affected by more and different factors than the oil majors.)

These sorts of actions should be on your “short list” of ways to get involved and have an impact.

Next Up: Investing and ESG

In the next and final segment of this three-part series, I will talk about the other side of the divestment coin, which is INvestment – the other financial lever we can use to change behaviors. And I’ll give you as concrete example of how I personally have used investment to support the battle against EACOP.

If precision INvestment strategies can get as much traction as DIvestment and ESG, multiplier effects will continue to compound the effectiveness of exercising financial power. See you there!

If you have made it this far, I want to sincerely thank you as I feel personally passionate about effectively wielding financial power in the fight for the climate.

I hope that readers come away with new appreciation for the need to expand our definition of divestment and update divestment programs to reflect lessons learned. This can help individuals make better decisions about supporting organizations or how to manage their own assets.